- Making Sense of Your Money

- Posts

- 🎉 Earning too much for a Roth IRA? Here’s how to (legally) do it anyway.

🎉 Earning too much for a Roth IRA? Here’s how to (legally) do it anyway.

Learn the loopholes of Roth IRA contributions.

Dan Pascone

April 11, 2024 • Read time: 8 minutes

Welcome to another edition of Making Cents of Your Money, where we dive into the nooks and crannies of financial strategies that matter to the time-constrained tech savvy.

Today, we're exploring the enigmatic world of the Backdoor Roth IRA, a strategy that's become a lifeline for high earners who are unable to make direct Roth contributions.

Here's why Backdoor Raths could be a game-changer for your wealth-building endeavors and what you’d need to do to get started– all in less time than it takes to order a double-chicken + guac bowl at Chipotle.

🔑🚪 Created in 1997, the Roth IRA was a game-changer.

Compared to the “taxes later” retirement savings vehicles like 401(k)s and Traditional IRAs, the “taxes now” Roth IRA allowed people to contribute after-tax dollars, and the accounts would grow tax-free.

Yes, you read that correctly. Any capital gains or dividends your investments earn within the Roth IRA grow tax-free. You don't have to pay taxes each year on capital gains, dividends, or interest within the account, and when you turn age 59½ (and have held the account for at least five years), you can make tax-free withdrawals.

Roth IRAs are particularly popular among folks who believe taxes will be higher in the future than they are today.

✅ It’s like leaving a very nice retirement present for yourself—no strings attached.

The Roth is powerful, especially for people retiring early because they can draw from it tax-free for life.

However, the ability to make direct Roth IRA contributions phases out at $153,000 Modified Adjusted Gross Income (MAGI) or $228,000 for married couples filing jointly.

🚪 Enter the Backdoor Roth IRA

The Backdoor Roth is a clever financial strategy enabled by the removal of income limits on Roth conversions in 2010. It allows high earners to sidestep direct contribution restrictions, necessitating meticulous attention to regulatory details.

It’s not an IRS piece of legislation but a tax workaround that the IRS and Congress are aware of but haven’t made any specific efforts or condemnations to close.

Functionally, the Backdoor Roth is a two-step dance. Sounds simple enough, but it requires meticulous attention to detail, and tiny missteps could inconveniently nip away at your dreams of a stress-free and tax-free retirement.

The two-step tango is as follows:

Kick off the financial ballet by contributing to a traditional IRA. This move is inclusive, with no income ceiling to hold you back. Whether your contribution is deductible or not is a sidebar in this performance—the main act is setting the stage for the Roth conversion.

Now, for the grand pivot: convert your traditional IRA to a Roth IRA. This is where the magic happens.

Now, here’s where the paths can begin to drift:

If you contribute pre-tax dollars into a Traditional IRA and then convert it into a Roth, you pay tax upon the conversion. Yes, you will have to pay taxes on the conversion at current ordinary income rates—but that’s just how Roth IRAs work.

If you contribute post-tax dollars into a Traditional IRA and then convert it into a Roth, you do not pay tax upon the conversion, and you don’t need to worry about the pro-rata rule below unless you had a prior Traditional IRA balance.

And– voila! Backdoor Roth IRA. You’ve transformed your retirement vehicle from “taxes later” growth to tax-free growth since you’ve already paid your fair share of taxes.

🙃 If only it were that simple in practice, though!

The Backdoor Roth IRA isn't without its hurdles, featuring complexities like the "pro-rata" rule.

⭐ Definition: The “Pro-rata” Rule: When you convert any portion of your Traditional IRA (which contains both pre-tax and after-tax contributions) to a Roth IRA, the amount converted is considered to come proportionally from your pre-tax and after-tax balances. This means you can't just convert the after-tax portions to a Roth IRA without also converting some pre-tax money, which would be taxable.

Suppose you have both pre-tax and after-tax funds in the same Traditional IRA and wish to convert to a Roth IRA. The IRS doesn’t allow you to convert only the after-tax funds– no cherrypicking!

The IRS's pro-rata rule essentially mixes the pre-tax and after-tax funds together for the purposes of conversion and taxation.

Also known as the "Cream in the Coffee" rule, the “pro-rata” rule outlines that once you mix non-deductible contributions (the cream) with the total funds in your IRA (the coffee), they become inseparably integrated.

Each withdrawal or conversion you make thereafter contains a proportionate blend of taxable and non-taxable amounts, akin to every sip of coffee having a bit of cream.

Simply put, this creates a (potentially avoidable) tax headache, as every withdrawal you make upon retirement has some taxes and accounting built into it—forever yours to account for and pay.

📊 Tax Implications: If you proceed with a conversion, you will owe income tax on the pre-tax portion of the conversion. The after-tax contributions convert tax-free since those funds were already taxed. However, determining the taxable amount involves calculating the ratio of your after-tax contributions to the total IRA balance (including all your IRAs, not just the one being converted).

🤔 The difference between a 100% tax-free withdrawal retirement and a 99.9% tax-free withdrawal retirement is way too big– maybe not financially, but mentally.

You’ve worked your entire life planning for a stress-free future, so why keep a recurring to-do list item indefinitely if you can avoid it?

Backdoor Roths also require excellent recordkeeping—specifically, IRS Form 8606, the proper filing of which ensures you don’t pay taxes twice on the same dollar.

Pssst... Considering a Backdoor Roth IRA? Start with our complimentary Financial Analysis. Click here: Free Financial Analysis - Online scheduling to see if the Backdoor Roth strategy (or something else) is a fit for you.

Making Cents of Backdoor Roth IRAs

🤸Why bother with this financial gymnastics? The benefits are too juicy to ignore.

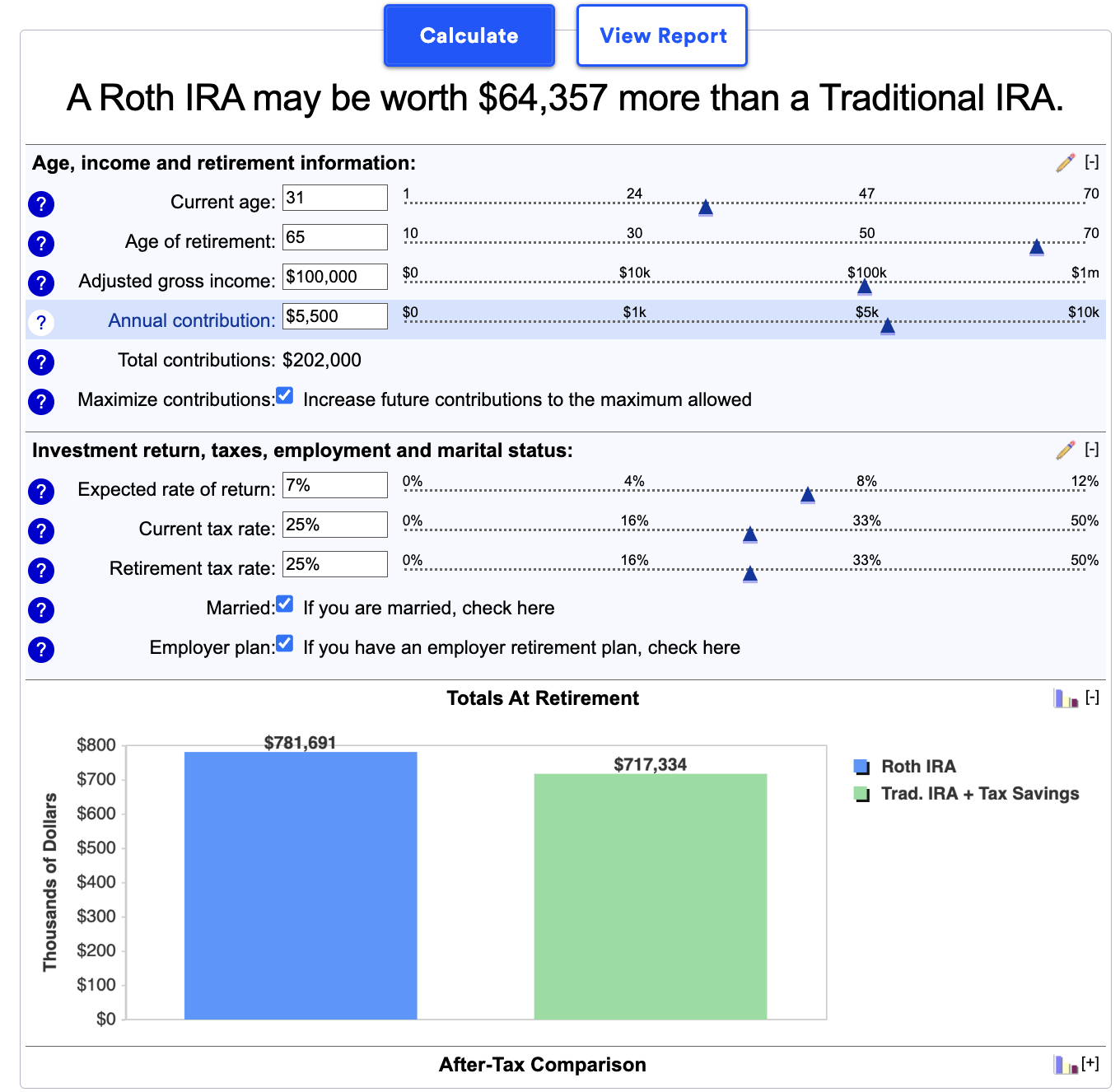

For example, filling out this Bankrate calculator with arbitrary figures, the Roth IRA beats out the Traditional IRA + Tax Savings from credits by $64,357– assuming the retirement tax rate is the same as your current tax rate.

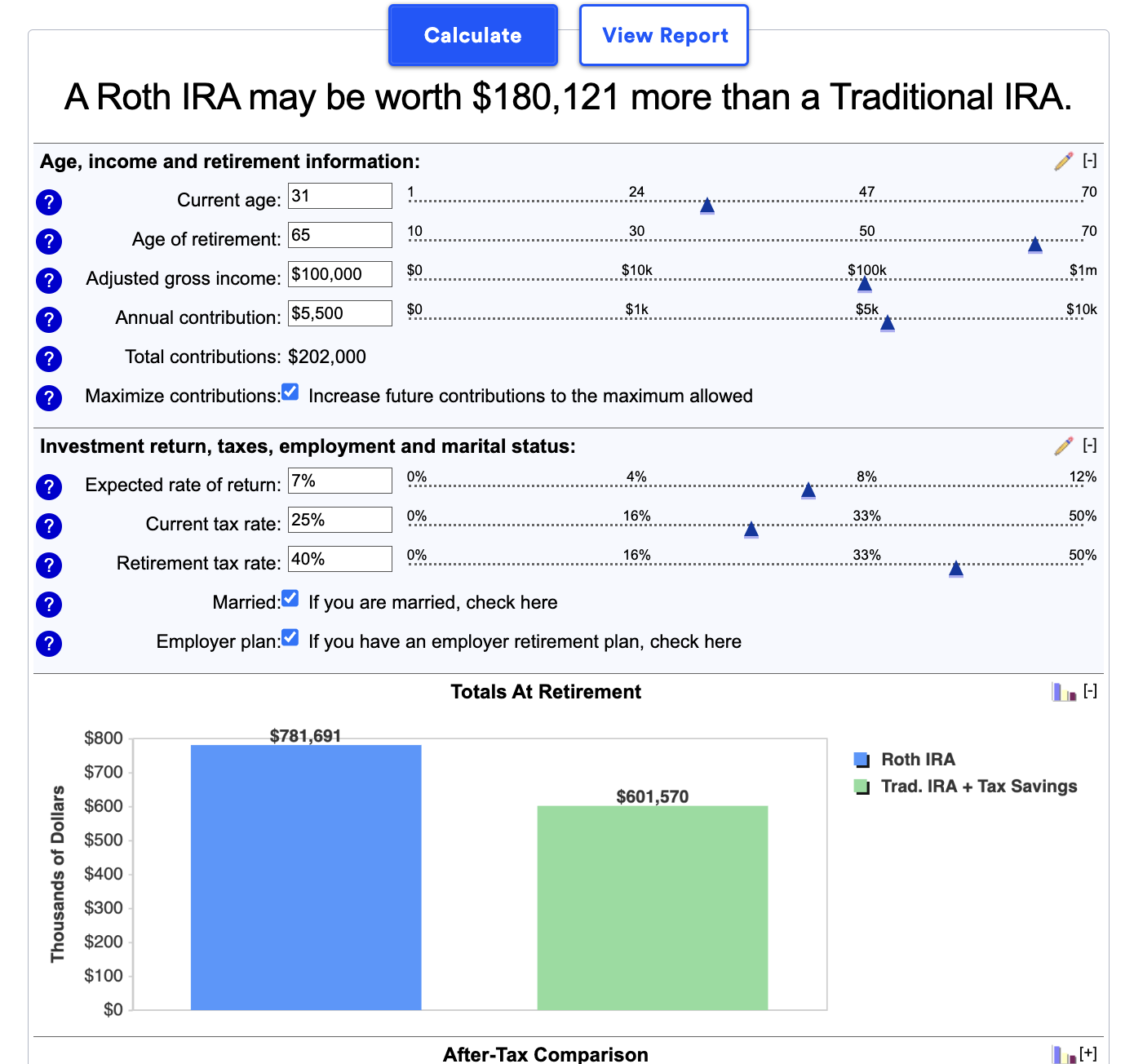

While some may anticipate a lower tax rate upon retirement (no or lower income upon leaving your job), Roths take the lead if tax rates are higher.

For instance, if your retirement tax rate is 40%, a Roth IRA is worth a whopping $180,121 more than a Traditional IRA using the same criteria.

“But, Dan, let’s be real. A 40% tax rate would be crazy; there’s no way taxes would be higher than today’s rates.”

Here’s the thing.

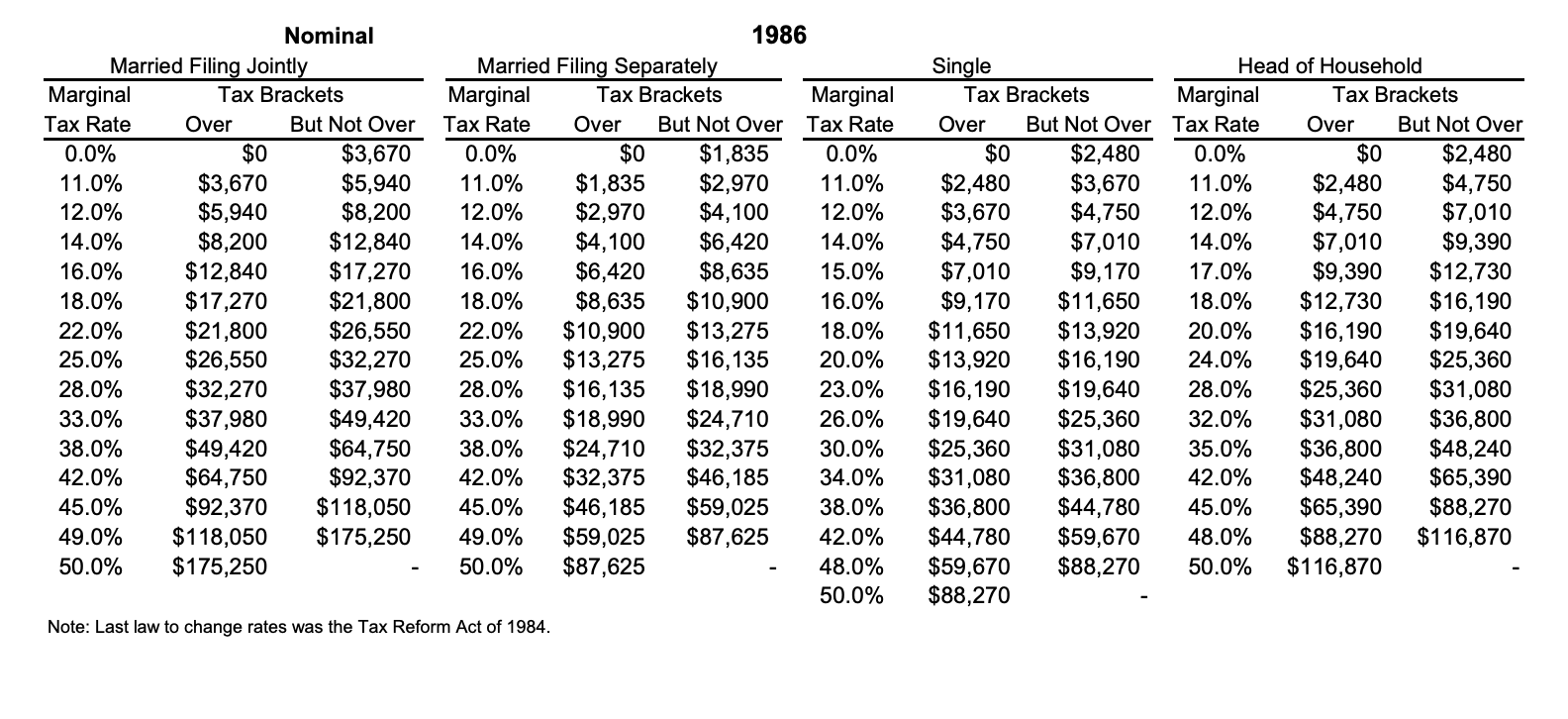

While today’s taxes seem high– and certainly do sting– historically, they’re some of the lowest.

The highest marginal tax rate in 1986 was 50%. In 1980, it was 70%. We even saw as high as 94% during and after WW2 in the 1940s and 1950s.

Folks predict higher tax rates in the future for many reasons, but let’s not get into that here. The point is that paying today’s tax rates when converting to a Roth may shield you from potentially higher rates.

As we wrap up, consider if a Backdoor Roth IRA aligns with your financial goals and timelines.

The intricacies may seem daunting, but they’re more of a call to action to work with highly credible financial planners– and, more importantly, ensure they’re in communication with the rest of your financial team, like a CPA, if you have one.

Until next week, stay savvy!

Dan from Tailored Cents