- Making Sense of Your Money

- Posts

- 🔮 Future-Proof Your Retirement: Pre-Tax vs. After-Tax Accounts & Tax Diversification

🔮 Future-Proof Your Retirement: Pre-Tax vs. After-Tax Accounts & Tax Diversification

Breaking down the tax implications of all retirement accounts

Dan Pascone

June 05, 2024 • Read time: 8 minutes

☕Good morning!

From the moment we cash in our first paycheck to the last (and beyond), we’re haunted by the tax bogeyman.

This week, we’re making taxes upon retirement less scary by shedding light on tax diversification and how the two primary approaches to retirement accounts (pre-tax, tax-deferred accounts and after-tax, tax-free accounts) can set you up for a stress-free retirement.

Here's the skinny: Some retirement accounts tax your money upfront—convenient now, but you’ll pay later. Others let your money grow tax-free until you withdraw it—you might feel the tax burn today, but you’ll thank yourself in the future.

Let’s get into it.

🎉 Pre-Tax, Tax-Deferred

So, you’re keen on the “pay it later” approach.

You could get a tax credit upfront. The Saver's Credit is a government incentive to encourage saving. The credit amount is based on your income level and the amount you contribute, with a maximum credit of $1,000 for married couples filing jointly and $200 for single filers (with phase-outs at higher income levels).

Your contributions to accounts like Traditional IRAs may be tax-deductible depending on your income and filing status.

This can be a significant advantage if you’re in a high tax bracket today and are in a lower one upon retirement.

However, when you eventually withdraw the money in retirement, it will be taxed as ordinary income.

Suppose you retired from your main gig today.

While you wouldn’t have a salary to add to the lump sum, your ordinary income would still include interest income from savings accounts, CDs, money market accounts, bonds, dividend income, profit distributions from companies you own stock in, rental income, royalties, and side hustle income.

Let’s say all of this adds up to $120,000, placing you in the 24% tax bracket.

That means you’d pay 24% on every dollar from your tax-deferred accounts.

It’s not usually a problem if you’ve planned for it ahead of time, but it can be a nuisance that can potentially push your retirement date back a few years.

Further, if tax rates increase across the board (not just your ordinary income activities), you could end up paying the higher tax rates upon retirement.

That 24% could, hypothetically, be 40% or higher when you actually retire, which could create an inconvenient situation.

Also, accounts such as the Traditional IRA require you to wait until age 59 ½ to take penalty-free withdrawals, and you are required to begin taking Required Minimum Distributions (RMDs) at age 72 (70 ½ if you were 70 ½ before January 1, 2020.)

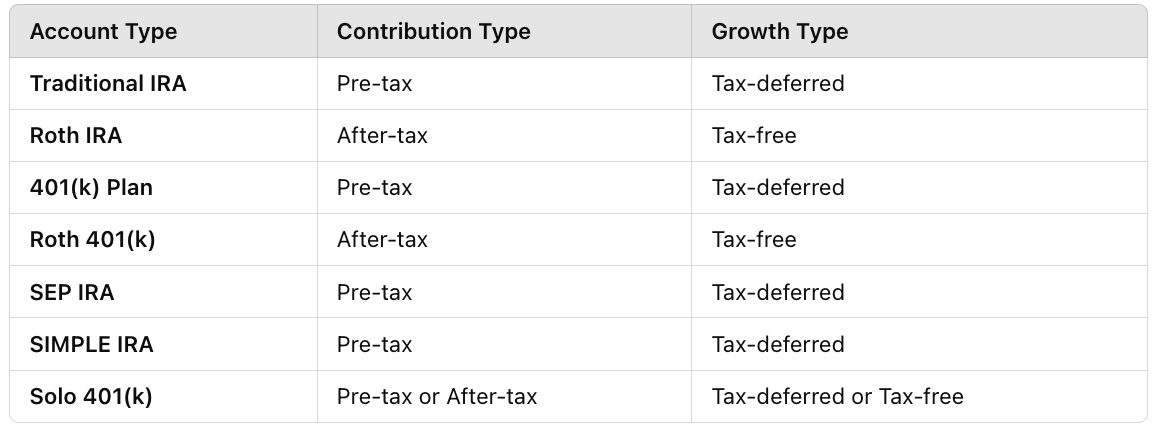

📈 Popular Pre-Tax, Tax-Deferred Accounts:

Traditional IRA: A flexible option for individuals, offering a contribution tax deduction.

401(k): Many employers offer these employer-sponsored plans, allowing you to contribute pre-tax salary with potential matching contributions from your employer. In most cases, this is a “no brainer” as it’s free money.

SEP IRA: Ideal for self-employed individuals and small business owners, SEP IRAs offer high contribution limits and tax-deferred growth.

SIMPLE IRA: Another option for small businesses with up to 100 employees, SIMPLE IRAs allow both employer and employee contributions with tax-deferred growth.

🤔 Important Considerations

Tax Implications: Remember, you'll pay taxes on the money when you withdraw it in retirement.

Contribution Limits: Each account has specific contribution limits, so be sure to research and stay within them.

Withdrawal Rules: There are typically penalties for withdrawing funds before a certain age (usually 59½).

After-Tax, Tax-Free

This approach involves planting a seed today and letting it grow to its full potential tax-free until retirement.

While you don’t get a tax deduction, this “pay now, tax-free later” approach is a powerful way to build a predictable nest egg in the future.

Here, you contribute money already taxed, and any earnings on your contributions, like interest or dividends, accumulate tax-free. This can be a significant perk if you expect to be in a higher tax bracket (or if taxes are generally higher) when you retire.

Similar to pre-tax, tax-deferred accounts, contributions to after-tax, tax-free accounts may still qualify for the Saver's Credit.

Suppose you’re in the 24% tax bracket today. You could contribute after-tax dollars to a Roth IRA, and then your contributions grow tax-free within the account.

When you retire and withdraw the money, assuming you meet the IRS qualifications for a qualified withdrawal, you won't owe any contributions or earnings taxes.

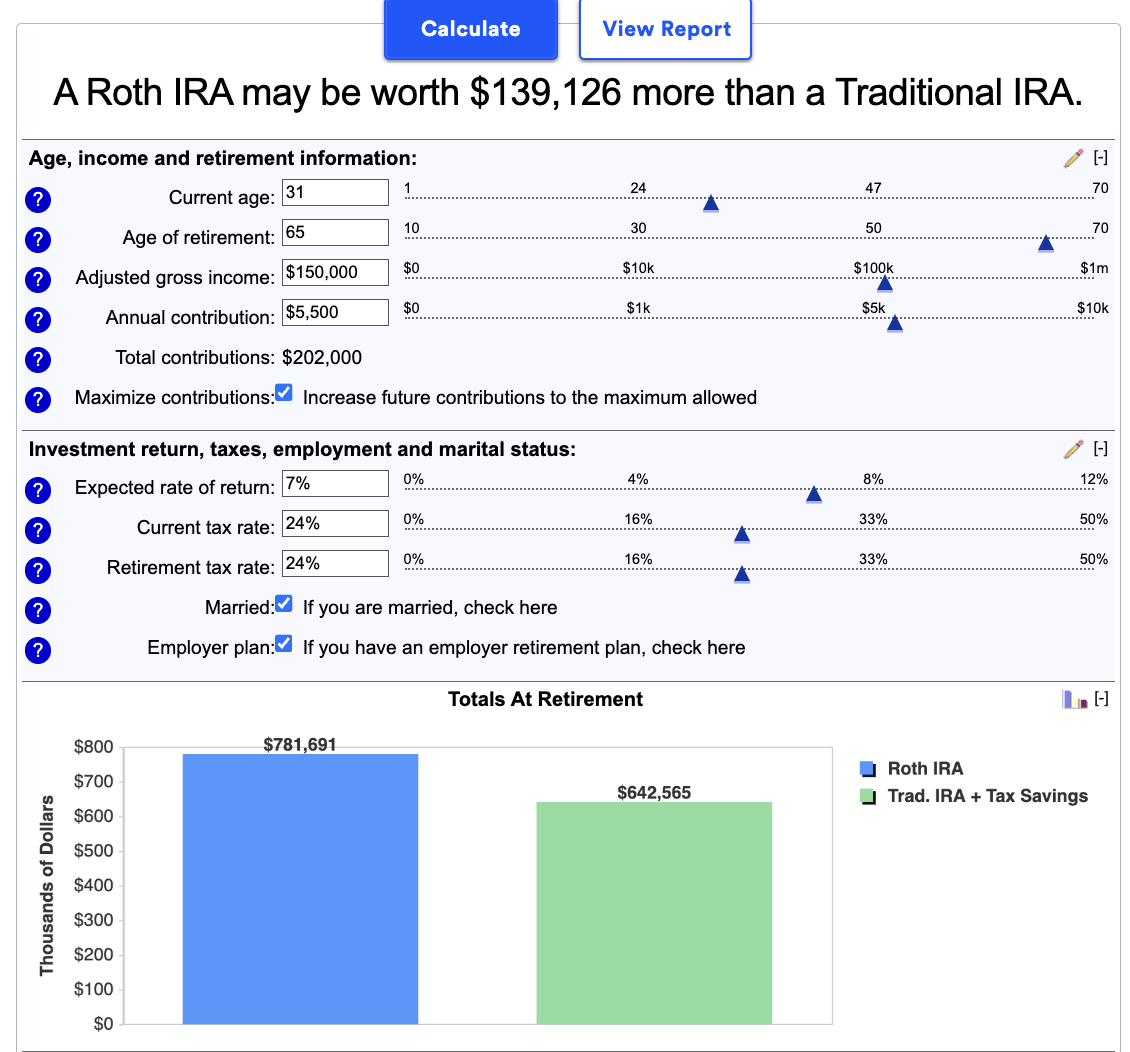

Let’s walk through the following example to visualize the difference.

For the Roth IRA, this is the account's total value. For the Traditional IRA, this is the sum of two parts: 1) The account's value after you pay income taxes on all earnings and tax-deductible contributions and 2) additional earnings from the re-invested tax savings.

You begin contributing to a Roth IRA at 31 at the maximum annual contribution limit. Assuming you have the same tax rate today and at retirement, you’d still have about $139,126 more in your Roth than in the Traditional IRA, considering the same 7% expected rate of return in both accounts.

This formula doesn’t take into account the tax deductions from the Traditional IRA you get today, but still, if we just focus on the nest egg, a Roth IRA has its clear advantage.

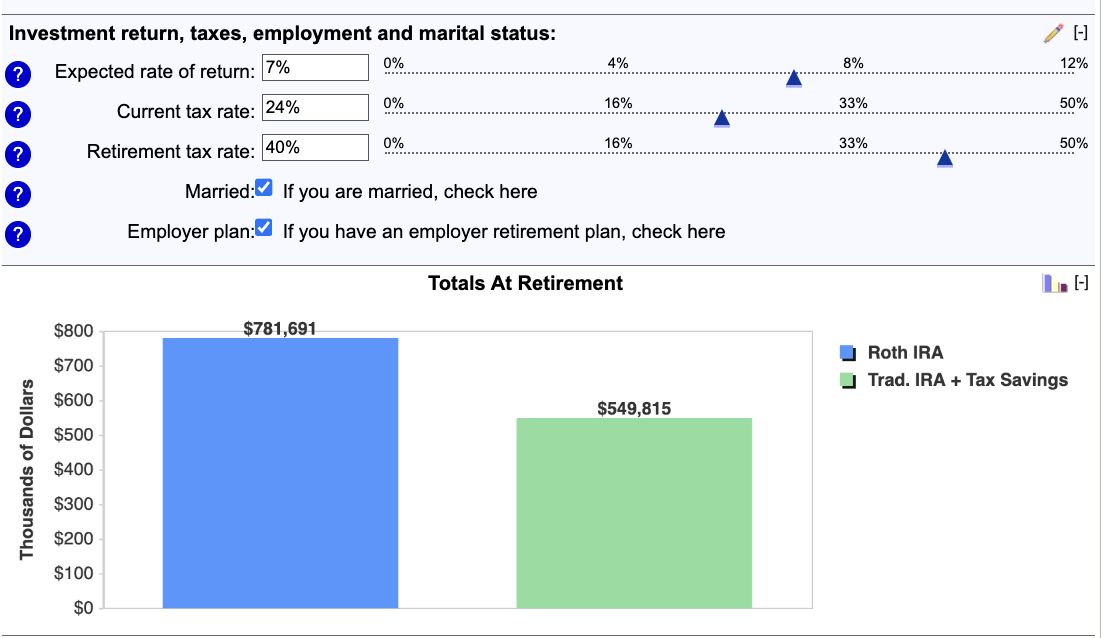

However, if the government increases tax rates across the board and your retirement tax rate increases to an arbitrary 40%, you’d have roughly $100,000 less in your retirement account.

If taxes are higher (40%), your Traditional IRA becomes much less effective.

📈 Popular After-Tax, Tax-Free Accounts:

Roth IRA: A flexible option for individuals that can be done through popular brokerages like Vanguard.

Roth 401(k): Some employers offer Roth 401(k) options, allowing you to contribute after-tax salary with tax-free growth and qualified withdrawals.

🤔 Important Considerations:

Tax Implications: Remember, the tax advantage here is on the growth within the account, not an upfront deduction on your contributions. You've already paid taxes on the money you contribute.

Contribution Limits: There are still contribution limits for after-tax, tax-free accounts. As of 2024, the combined limit for all your IRAs (both traditional and Roth) is $7,000.

Withdrawal Rules: Qualified withdrawals from Roth IRAs and Roth 401(k)s are tax-free and penalty-free if you meet specific requirements, like reaching age 59 ½ and holding the account for at least five years. There are exceptions for certain circumstances, like using funds for a first-time home purchase or qualified medical expenses.

🎭 Making Cents of Retirement Accounts: Tax Diversification

No one has a crystal ball to predict future tax rates, and using a mix of pre-tax and after-tax accounts can be an intelligent strategy to guarantee a tax-happy retirement.

If tax rates are lower, you'll benefit from the tax-deferred growth of pre-tax accounts. You get the tax savings today and the lower taxes in the future– win-win!

If your withdrawals are higher, you’ll have tax-free withdrawals to save the day. Remember, the tax advantage here is tax-free growth, not an upfront tax deduction—no tax relief today for significant relief later.

There are still contribution limits for after-tax, tax-free accounts, so research and stay within them. For example, in 2024, the total amount you can contribute to all your IRAs (both traditional and Roth) is $7,000, whereas the employee contribution limit for 401(k) plans is $23,000.

Tax diversification is about hedging your bets and giving yourself flexibility depending on your tax situation when you finally decide to retire, and most importantly, preventing things outside of your control, like the government choosing to raise taxes, rain on your parade.

Until next week!

Dan from Tailored Cents

P.S. Follow me on LinkedIn for more tax gems to save you money.